Published on

Tuesday, June 30 2020

Authors :

Julia Tossetti and Sam Davis

Despite the pandemic, interest in renewable fuels continues to grow. This is largely because government mandates drive its demand, which is expected to continue increasing as carbon-reduction policies reach greater stringency. This is already visible at the federal level, as well as at the state and regional levels, and it is one aspect of this week’s blog: examining the drivers of renewable fuel demand. Equally important is addressing the basics of renewable fuels. What types of renewable fuels are there? What are they made from? What factors determine their market value? Answers to these questions are explored this week and will be examined more closely in subsequent blogs.

Part I: The Drivers

Policy governs the production and consumption of renewable fuels. Left strictly to market forces, these fuels would be overshadowed by petroleum because the latter has economic advantage. So why are alternative fuels used if they are more expensive to produce? Why do governments require their consumption? The answer lies in climate change. While at an economic disadvantage, renewable fuels offer sources of energy that produce fewer greenhouse gas (GHG) emissions relative to petroleum fuel. GHGs have a unique property of absorbing infrared radiation (i.e., heat waves) and reradiating it, and the pronounced effects of this phenomenon contribute to global warming. This is why governments craft policies to decrease GHG emissions: to reduce the amount of infrared reradiation and, by extension, temperature elevations that can become detrimental.

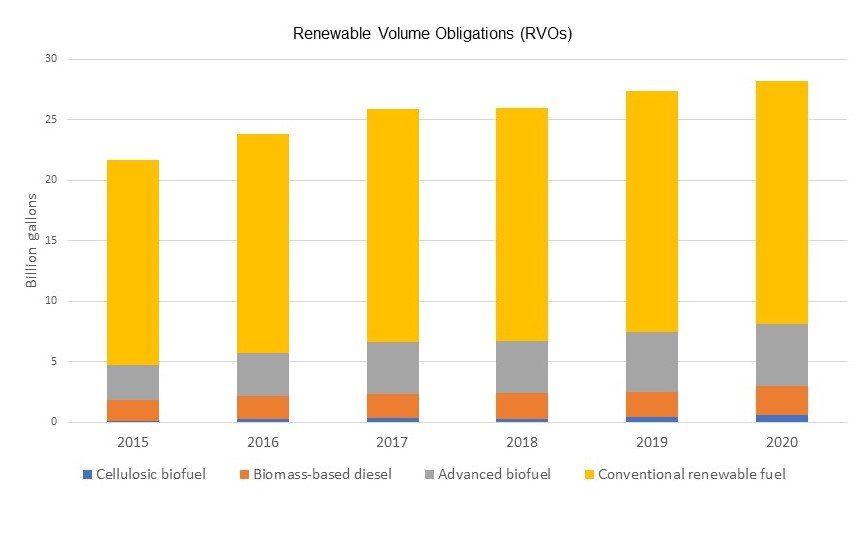

Here in the United States, the federal government oversees the usage of renewable fuel through the Renewable Fuel Standard (RFS). Originally implemented in 2005, then expanded in 2007, the RFS designates yearly volumes of renewable fuel to be blended with petroleum-based transportation fuel. Broadly speaking, parties that produce and import gasoline and diesel fall under the RFS’ purview and must demonstrate compliance with it each year. The following renewable fuels are covered by the RFS: conventional renewable fuel, advanced biofuel, biomass-based diesel, and cellulosic biofuel. Each year, the Environmental Protection Agency (EPA) sets renewable volume obligations (RVOs) for each fuel type. Figure 1 shows graphs of the RVOs dating from 2015. The yellow bars representing conventional renewable fuel correspond to the corn ethanol that is blended into our gasoline: approximately 10% by volume. More will be said about the remaining fuel categories later in this blog and in subsequent ones.

Figure 1

Some states and regions are undertaking their own GHG reduction programs. The most well- known and mature of these is the California Low Carbon Fuel Standard (CA-LCFS), which is administered by the California Air Resources Board (CARB). Approved by CARB in 2009, the regulation has created a bustling, incentivized marketplace that attracts renewable transportation fuel from all over the world. The CA-LCFS program will resurface in later blogs, as it is a very prominent component of the renewable fuel industry.

Part II: The Basics of Renewable Fuel

When thinking of renewable fuel, one tends to think of energy sources that are not petroleum-based: corn ethanol, biodiesel, and biogas, to name a few. The unifying factor among these fuels is their basis in biological matter; they are made from what is collectively known as biomass. Biomass can refer to crops that are grown specifically for use in renewable fuel production. It can also mean biological matter that is generated as waste through the production of something else; stover, used cooking oil (UCO), and animal fat (tallow) are by-products of agricultural, food, and meat production, respectively. This means extra resources are not required to make them, as they already exist. Furthermore, they do not compete with the land, water, fertilizer, etc. that are required for food production.

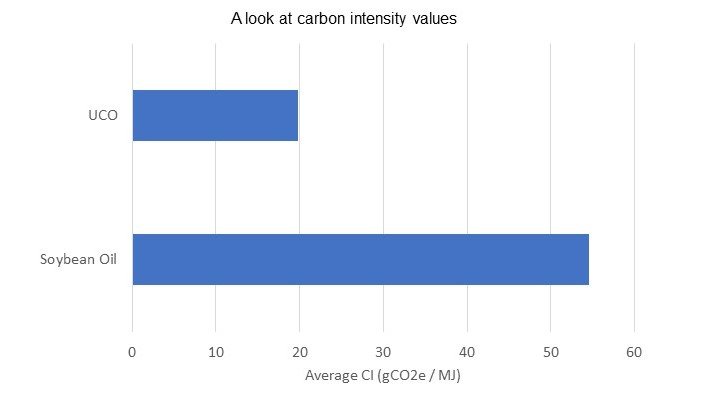

It should start becoming apparent that there are two broad categories of biomass that make up renewable fuel inputs, or feedstocks: crop and waste. The designation is crucial because there is a significant difference between their value in the marketplace. Recall that the whole point of producing and consuming renewable fuel is to reduce GHG emissions. The enormous question that scientists have to address is, how does one truly quantify these emission reductions? The emissions of a vehicle’s tailpipe are simple enough to measure; but they do not tell the whole story. There are also GHG emissions caused by the production and transportation of renewable fuel. In order to accurately measure GHG reduction, the energy inputs required to make and distribute these fuels must be accounted for. Instead of a simple tailpipe measurement, an energy balance becomes necessary. This holistic approach is known as the life cycle analysis (LCA). Through its application, there is a way to quantify the GHG emissions of fuel starting at its production and ending with its consumption. This quantification is called the carbon intensity (CI) value. It is a single number given in units of the quantity of carbon dioxide emitted per unit of energy consumed.

Crop and waste-based feedstocks differ appreciably in their market value. With an awareness of CI, one can start to grasp why. Between crop and waste, which one generates more GHG emissions as it is produced? Consider a gallon of soybean oil and an equal amount of UCO. To obtain the soybean oil, one must first grow soybeans. Then they need to be harvested and processed to extract the oil. Now, think about the gallon of UCO. It does not require its own process to become a feedstock; it already is a feedstock. It just needs to be collected from restaurants. These are simplified scenarios, but hopefully the point is becoming clearer; waste-based feedstocks for alternative fuels are more valuable than crop-based ones because they require less energy to produce. In other words, fewer GHGs are emitted during their production. By extension, it follows that the fuels made from waste feedstocks have lower CI values than those made from crop. This is indeed the case, as Figure 2 illustrates.

Figure 2

The RFS was mentioned earlier, as well as the different renewable fuels that fall under it. One of these, biomass-based diesel, has created a lot of interest in recent years and continues to do so. To further understand the basics of this renewable fuel, consider a few aspects of nomenclature. Biomass-based diesel is the umbrella category for biodiesel and renewable diesel. There are differences between the two. While both can be made from fats and oils, renewable diesel can also be produced from agricultural and forestry residue. Another important difference is production; the feedstocks undergo different treatment, depending on which biomass-based diesel is needed. Lastly, there are several differences in how the diesels perform in engines and interact with existing fuel infrastructure.

This blog began by discussing why and how the federal government regulates renewable fuel. Next, it gave an introduction to renewable fuel feedstocks, how they are categorized as either crop or waste, and why these differences matter in the market. Lastly, we defined biomass-based diesel and its two subcategories, biodiesel and renewable diesel. With these basics, one can start to examine the renewable fuel realm a lot more closely, and the market’s enthusiasm for it, which we aim to do in future blogs.

Turner, Mason & Company has been active in the renewable diesel market for the past 10 years through single and multi-client engagements including due diligence of renewable diesel facilities. In response to growing market interest, our team is currently assessing renewable diesel market opportunities created by the various blending mandates, through the development of market research aimed at analyzing future supply and demand of renewable diesel, quality and sustainability of feedstock supply, and the economics driving existing plant conversions and new builds. For more information about our renewable diesel market research or for any specific renewable fuels consulting engagements, please visit our website: https://www.turnermason.com and send us a note under ‘Contact’ or give us a call at 214-754-0898.